Airtel Africa (AAF:LSE) Deep Dive - A Striking Opportunity from Sub-Saharan Africa

Currency troubles in Nigeria have pummelled AAF's earnings and raised questions about future prospects - but few companies remain better set to benefit from the coming African economic boom.

(I recommend clicking through to view this post on Substack if you received this as an email, as the graphs tell a big part of the story here.)

Intro

Sub-Saharan Africa contains most of the youngest, fastest-growing and fastest-digitalising populations in the world. By 2050, Africa’s population is expected to reach 2.5 billion, from just 1.48 billion today, and the continent’s GDP is projected to grow from $3.1 trillion to $20-30 trillion. At the same time, smartphones are quickly becoming more affordable, and data usage among African smartphone users is skyrocketing. Additionally, financial exclusion and a massive unbanked population is causing mobile money usage to surge.

In the coming decades, many a fortune will be made by investors in Africa, and I believe few companies present such a striking long-term opportunity at such a reasonable price as Airtel Africa - the continent’s second-largest mobile network operator and mobile money provider. In this analysis, I’ll go deep into the economics, growth profile, risks and valuation of Airtel Africa, and attempt to convince you that the business represents excellent value at the current (Mar 09, ‘24) price of 95 GBp.

The author of this article has a financial interest in the company mentioned. The views expressed are for informational purposes only and should not be considered as financial advice. Readers are encouraged to conduct their own research and consult with a qualified financial advisor before making investment decisions.

On a related note, I’ve noticed a lot of investors seem to have developed a complete aversion to emerging markets as a result of their dismal performance over the past decade and a half (black is FTSE EM, blue is SPX):

These investors, many of them value investors, have concluded this is simply the way of the world - US stocks do better and always will.

History would beg to differ. While overall US returns have been better, the relationship has been cyclical. The US outperformed in the 1950s, 1980s, 1990s and 2010-present; EM in the 1930s, 1970s and 2000s. Strong decades for EM are typically followed by weak ones, and vice-versa.

The US’s recent record has of course not been entirely performance-driven - cyclically adjusted S&P500 multiples have expanded to levels only previously seen in 2021 and the dot-com bubble. Meanwhile, EM markets’ multiples have been virtually flat since the GFC, leading to a divergence of almost 2.5x - S&P500 at a Shiller PE of 34, versus EM at about 14. In my view, this has created some incredible opportunities in emerging markets (such as Airtel Africa) and I’d urge strongly investors not to shy away from these currently unloved markets - they may well be the darlings of the next decade.

By the way, this will be a pretty long one - probably a 30 minute read.

Business Overview

83% of AAF’s revenue is currently derived from their mobile networks, of which voice is the largest portion, with data quickly catching up. “Other” consists mainly of revenues from SMS, tower-sharing, and certain exclusive partnerships with Bharti Airtel). The business model is fairly simple - buy spectrum from the government, put a dish on a third-party-owned tower (usually - AAF own about 8% of the towers they use) and sell as many SIM cards as you can.

The remaining 17% is Airtel Money, which allows customers to use their mobile number as an electronic wallet. Airtel SIM holders who set up a wallet can send money to any other Airtel wallet, or wallets of other mobile networks (often with a slightly higher fee) by dialling a certain code and entering the recipient’s details, or by scanning a barcode. This is used for P2P, in-store and bill payments. In the most recent quarter, Airtel Money’s total transaction value was $29b.

East Africa - Tanzania, Kenya, Uganda, Zambia, Malawi, Seychelles

Francophone Africa - DRC, Niger, Chad, Gabon, Rwanda, Congo, Madagascar

Airtel Africa operates in 14 countries in the continent, giving them a reasonable degree of geographical diversification (though of course the economic health and prosperity of these markets are correlated). Nigeria is their most important single market by a wide margin, accounting for a third of revenue and 41% of operating profit. Their other top markets are DRC, Tanzania, Kenya, Uganda and Zambia.

Competitive Dynamics

Networks

Competitive dynamics between mobile network operators (MNOs) are characterised mainly by strong economies of scale and barriers to entry, for several reasons:

Tower overheads - a large portion of the costs of building and running a tower are fixed with respect to the number of customers it serves, or at least do not scale linearly (e.g., a dish that’s twice as expensive may be able to handle 4x the data). Thus, larger competitors can typically achieve a given network quality with lower capex intensity (capex/revenue) and higher operating margins.

Spectrum costs - similarly, larger players have to spend less per head on spectrum. This is both because required bandwidth scales less-than-linearly with data throughput, and because the cost of spectrum is often not proportional to the width. Spectrum is typically sold by governments in pre-determined sizes at auctions, where a slice may cost tens or hundreds of millions of dollars - a difficult situation if you’re a small player.

Geographical advantages - making incremental investments in coverage is typically more profitable for larger players, since not only do they capture a portion of the inhabitants of the area they expand into, but it also increases the areas available to existing customers. If a customer uses service in an area not covered by their MNO, the MNO must transfer them onto a competitor’s network and pay an interconnection fee to that competitor - so the greater an MNO’s coverage, the less it pays in fees.

Regulatory barriers to entry - the telecom industry is heavily regulated, with companies requiring many licences and permits, and facing compliance with quality standards and coverage commitments. This makes it a right old pain for any new entrants to even get up and running in the first place, before they face all the aforementioned issues.

TowerCo relationships - most MNOs rely on tower holding companies to own and operate their towers (for example, AAF only owns 8% of the towers they use) - larger players naturally have more power in this relationship to seek better prices.

The result?

New entrants into a telecom market are very rare, requiring a large financial commitment. Successful new entrants are even rarer.

Smaller players primarily exist in the largest cities, where population density can make up for their lower penetration rate and higher roaming fees

Aside from in those large population centres, smaller players have systemically underinvested in their networks due to lower capex returns; quality has not kept up with bigger players and they have gradually bled market share as a result

So where does Airtel Africa fit into the competitive picture?

In 5 of their 14 markets, they are the largest competitor; they place second in another 7. This scale has allowed them to make outsized networks investments (while keeping margins high), and as a result, their networks are generally superior, especially for data. Consequently, aggregate market share has been gradually increasing over the past decade (note that this chart only contains data for 10 of their 14 markets, but it covers 92% by population):

There are some interesting results if we break this down by country:

The countries in which Airtel had the highest market share in 2014 generally saw the worst performance over the decade. There are two main reasons - firstly, Airtel has generally been more willing to reduce investment in the markets where they are dominant, increasing free cash flow at the cost of competitiveness, and investing that cash into markets where competition is tougher. Secondly, regulators do not particularly like one company having a dominant share of the market, so are likely to incentivise competitors in some way if that is the case.

What this data doesn’t show is how a rising tide lifts all (big) boats - their customer numbers have doubled or more in 8 of the 10 markets shown, with the exceptions being Rwanda and the Congo. As for the small boats - time and time again, the smallest players have suffered in almost every market, and often withdrawn entirely.

There is another interesting takeaway from trawling through all the telecom regulators’ publications that doesn’t show up in this data - AAF is a definitively data-forward operator. Their coverage and performance statistics for calls are typically in-line with other market participants (and usually slightly worse than MTN in the markets where they compete); but in most markets, their average upload/download speeds blow competitors’ out the water. For example, in Uganda:

Indeed, Meta Portal reports that AAF have the highest average data speeds in 13 out of 14 markets. This has been a contributor to their positive market share performance, and as data becomes increasingly popular in Africa (current penetration among AAF’s customer base is ~40%) this driver will only become more impactful.

So the key takeaway is, size matters. Bigger is better. The only MNO larger than AAF in sub-Saharan Africa is MTN, a South African company with annual revenues of ~$10b (double AAF’s). The two companies compete in Nigeria, Uganda, Zambia, Rwanda and the Congo, with Airtel being larger only in Zambia. While I haven’t looked deeply into MTN, I currently prefer AAF due to their better management and more attractive markets; however MTN also trades at a very attractive valuation and it probably wouldn’t be unwise to hedge one’s bets by owning some shares in both.

Mobile Money

The competitive dynamics of mobile money vary significantly between countries - some require operators to allow payments between mobile networks with the same fees as between members of their own network; some allow higher fees when paying to a different network; and some don’t require any interoperability at all.

Kenya is an interesting example to look at. Prior to 2022, Kenya did not require interoperability; and while Safaricom already had a majority of the mobile network market share, this allowed their mobile money service, M-Pesa, to become completely dominant, with a market share of ~99% - there was little point using mobile money if you were with another provider, since you’d only be able to send money to a small minority of people. However, since 2022, operators have been required to offer the same fee structure on transfers regardless of receiving network, and by March 2023 - less than a year after the change - Airtel Money had already grown its market share to 3.4%.

One may expect that M-Pesa’s multiple decades of dominance would have driven customers towards Safaricom’s voice/data plans, but this has interestingly not been the case - their market share has been pretty flat, oscillating around 65%, since 2008. In the case of Kenya, mobile money offerings have not seemed to be a particularly strong driver when deciding which network to go with.

Broadly, I think countries will continue to move towards interoperability - regulators understand this is objectively better for consumers, and the main barrier has simply been technology. Consequently, mobile money subscriber numbers will become more and more just a function of overall SIM subscriptions, as network effects diminish.

The following chart shows Airtel’s fast rise to become the second-largest mobile money operator in Africa:

Business Quality

Telecoms are generally regarded as competitive, undifferentiated businesses with high capex requirements and low returns on capital. However, Airtel Africa doesn’t really fit this mould - in FY23, excluding losses on derivatives and FX, they made pre-tax profit of $1.37b. This represents a pre-tax return on tangible assets of 18%. One could debate the validity of removing all of those FX/derivative losses, but it stands that they do not earn a “normal” return for a mobile telecom.

Why is this possible?

The biggest factor is probably the scale advantages I described - many of Airtel’s competitors, who don’t have their scale, operate at returns on capital that are much more in-line with global norms.

Mobile money services also provide a good boost to profitability, as a high-margin product that requires minimal additional investment. As well as collecting transaction fees, they have $730m in float which they can keep in short-dated treasuries, likely earning >5% at the moment. Mobile money overall is currently at a $440m operating income run rate, so is far from insignificant.

Finally, as African markets are broadly high-risk, they require a higher return on investment to attract new capital, which allows a higher return for the incumbents.

Long-Term Growth Prospects

AAF’s prospects for long-term growth are excellent. They operate in some of the fastest developing countries in the world with young, rapidly growing populations (their Francophone segment has a median age of just 16 years old), rising smartphone affordability, low mobile data penetration and a large unbanked demographic. Aggregate smartphone adoption is just 37% in their markets, and only 41% of Airtel Africa’s customers use mobile data (despite AAF’s 4G alone covering 70% of their markets’ total population). The confluence of population growth, increasing smartphone adoption, and market share growth produces strong customer base growth; increasing penetration of data and mobile money within that customer base, and rising usage per customer have the potential to make revenue growth explosive. I’ll consider the trends in each of these factors, then multiply them together to estimate a sustainable medium-term USD growth rate.

Firstly, weighted average population growth (through 2025) of 2.7% sets a baseline to long-term growth. Next, while the average SIM adoption rate and market share numbers would take ages to find, the product of these - the aggregate percentage of the population in their 14 markets who are subscribed to an Airtel SIM - is easily calculable. It’s approximately 20%, and is growing consistently at 100bps per year, which is a 5% growth rate from AAF’s perspective (1%/20%).

Therefore, the customer base growth should approximate 8%.

Next, we need to consider the penetration and usage trends in each category to find their individual growth rates. Unfortunately, this section of the post will resemble a malt loaf - dense and dry - so feel free to skip to the “overall” part.

Voice

The penetration of voice among their customers is 100% - no one has a data contract with no calls, and you need a contract to use mobile money. And while usage per customer continues to rise (MRQ monthly minutes was 286, versus 184 in FY19), this has not been sufficient to offset currency depreciation, due in part to their strategy of not raising prices. Consequently, ARPU (average revenue per user) has fallen 4.2% annually since FY19. This implies a total voice growth rate of 3.5%.

Data

40% of their customers are on data plans, and this is rising ~200bps per year, contributing another 5%. Usage growth is excellent - up from 2.7GB/mo in FY21 to 5.5GB/mo in the quarter ended Dec ‘23. This has driven an ARPU increase from $2.5/mo to $3.0/mo as customers trade up (though it has recently dropped to $2.6 after the Naira crash - more on that later). I think it’s likely we will see ARPU continue growing, however for the sake of conservatism, I will assume flat ARPU. Consequently, we get 2.7% + 5% + 5% ≈ 13% data growth rate.

Mobile Money

25% of customers currently use mobile money, and this is also rising ~200bps/yr, contributing 8%. Monthly transaction value per customer is rising around 12.5% per year, while the average take rate is has dropped (due to a combination of actual rate lowering and increasing transaction size) from 0.94% in FY19 to 0.74% currently - 5% annually. Assuming this ARPU drop continues, we get 2.7% + 5% + 8% +12.5% - 5% ≈ 25% growth rate.

This is before accounting for the contribution of Airtel Moneey in Nigeria, which has already spread to >2 million customers fee-free after their license was granted in April ‘22, and will begin charging fees within “a couple of quarters”.

Other

No KPIs are given for their other revenue - the 4 year historical growth rate is ~9%, so we’ll just have to take that at face value.

Overall

Weighting by revenue, that gives a 10.5% growth rate. Of course, this would increase as the proportion of revenue from higher-growth areas increases, all else equal (11% the following year, 12% the next), but we’ll assume this is commensurate with the gradual decrease in growth rates they’re bound to see.

The Naira Devaluation

Here, we get to the crux of why Airtel Africa is at such depressed prices currently. Nigeria is by far their largest market, accounting for 40% of operating profit in 2022… and their currency, the Naira, has lost over 70% of its value in the last 12 months, going from an exchange rate of 460 NGN/USD to 1600.

Nigeria had been experiencing dollar scarcity for a while before the devaluation. While there are many reasons for this, it effectively boils down to supply and demand. Foreign businesses operating in Nigeria need to repatriate income, which usually means exchanging it for dollars; and local businesses and individuals have little faith in the Naira themselves, so will take dollars whenever they can - therefore, high demand. On the supply side, strong trade surpluses due to oil exports had been a key source of USD over the past 2 decades, but with a massive surge in oil theft, as well as general underinvestment in oil infrastructure, production has fallen from over 2 million bpd to less than 1.5 million over the last 12 years. Combined with low oil prices during the pandemic, this resulted in significant trade deficits over the past few years, replacing a historical source of dollars with a sink.

Nigeria scraped by for a few years by introducing a complicated exchange rate system, with multiple different rates depending on the transacting parties and purpose of the transaction. However, this was never really sustainable, and by June 2023, the liquidity crisis had become severe enough that the Central Bank of Nigeria (CBN) decided to move to a floating-rate regime.

This chart shows the result (it’s in Naira per USD, so bigger number means lower Naira value). Despite the immediate fall to around 800 NGN per USD, liquidity failed to ease up, and a massive slide to 1600 occurred at the beginning of February.

In total, that’s a fall of 71% in just 8 months. It goes without saying the impact on the top and bottom line will be severe - we’ll estimate this later. However, two things are important to point out here:

The devaluation is probably, mostly, over. Fair value estimates for the Naira tend to put it around 860-1000 per USD12, and the CBN’s estimate is, unsurprisingly, even higher at 650-750. Also, Nigeria’s Dangote refinery (one of the largest oil refineries in the world) was shut down in early 2023 alongside a few smaller refineries due to oil theft, but it has just begun operating again, and should be at full capacity (650,000 bpd) within a few months. This should be enough to meet all of Nigeria’s gasoline, diesel, kerosene and jet fuel needs3, reducing USD demand significantly as they no longer need to import these fuels. Finally, oil exports are on the rise again, which should ease the trade deficit.

The impact on gross/EBIDTA margin is not expected to be significant, because only 7% of their Nigeria OpEx is dollar-denominated. This has panned out so far, with their EBITDA margin in Nigeria actually increasing YOY in the quarter ended Dec 31 2023, from 51.8% to 54.9%. This move was not standard procedure among telecoms, and has actually put Airtel in a strong position relative to their competition, with an anonymous representative from one of the Nigerian competitors saying “We are earning in Naira and about 80% of our costs are in dollars. There’s no way we can have a sustainable business without increasing our prices with the value of the Nigerian currency falling every day.”4

Finance Costs

If we are analysing the business from a USD perspective, as we have when looking at growth, the revenue and EBIT drop is just about the end of the story as far as negative impacts go*. And in fact there’s a benefit we haven’t yet noted - some of their debt is denominated in Naira (they don’t disclose exactly how much). That debt just got a whole lot less valuable, in USD terms.

However, if we look at the business from a local currency perspective, the opposite is true. Any debts denominated in USD just became worth a whole lot more, in Naira terms.

The way Airtel Africa’s accounting works is each of the local subsidiaries reports in their local currency, then all the income (and cash flow) statement items are translated at the average USD exchange rate over the period, in order to consolidate them onto the parent company’s income statement. On the other hand, the balance sheet items are translated at the end-of-period exchange rate. This results in two recorded losses - one under “exchange loss due to USD liability translation” ($471m, Mar-Sep ‘23), often included within finance costs; and one under “loss due to foreign currency translation differences” ($628m) - annoyingly similar, I know - within other comprehensive income.

However, from our USD-based perspective, I think we can completely ignore these “expenses”. If you’re not convinced, consider that if the USD-reporting parent company instead held those USD-denominated debts - as it does for some of them - there would be no loss recorded at all, despite that being an identical position in practice (aside from any tax differences).

* Okay, so not quite. They’ve also recorded some significant derivatives losses ($184m, Mar-Sep ‘23), which may seem weird since you’d think they should be hedging their currency losses. The reason for these losses goes back to the liquidity problem - some of their suppliers only accept USD, and in order to get hold of those dollars, AAF was forced to enter into a contract alongside the currency exchange wherein they take on the Naira currency risk. These will eventually materialise as a cash expense, assuming the currency doesn’t appreciate, so should be taken into account; but at 1600 NGN per USD, there’s simply not that much further to fall, so future derivatives losses will likely be minimal.

Management and Ownership

Ownership

The main thing you need to know about the ownership is it’s 74.23% owned by Bharti Airtel, the Indian parent company, meaning they have ultimate power over the board and executive team. Airtel Africa’s chairman, Sunil Mittal, is the founder and chair of Bharti Airtel, and his son is also on the board. Bharti’s vice chairman also sits on the board of AAF.

No other shareholders have an influential stake.

Management

In June 2024 Segun Ogunsanya will retire as CEO, a position he has held since 2021 - before which he managed Airtel Nigeria for almost a decade. He will be replaced by Sunil Taldar, an Airtel exec.

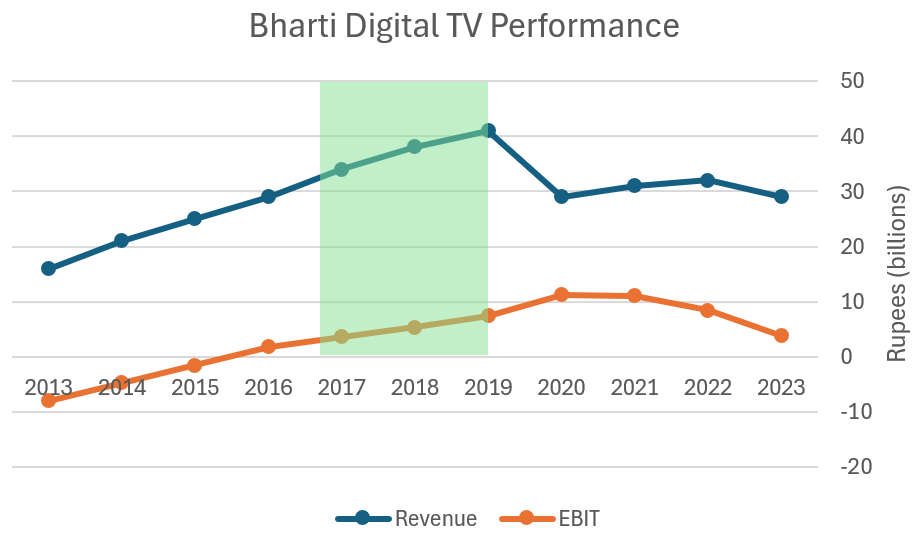

Sunil Taldar began his career at Mondelez (Cadbury) in 1996, gradually climbing the ranks from a branch manager in India to become managing director of Modelez Indonesia by 2015. In 2016, he moved to Bharti to become CEO of the direct-to-home (DTH) TV division. 2 years later, he moved to the “homes” division (broadband, fixed telephony), again as CEO, then in 2021 was promoted to Bharti Airtel director of operations. While he was not in any of these positions for long enough to get a definitive idea of his impact, it’s worth looking at their performance:

The period for which Taldar managed the businesses is highlighted - in both cases, it’s clear there was an improvement in performance during and in the couple years after Taldar’s management (the drop in revenue in the first chart in 2020 is due to a regulatory change - EBIT still increased significantly). This record goes some of the way to explaining why Taldar, who has no management experience in either mobile services or Africa, was chosen for the CEO role.

On the personal side, there’s not a lot to say about him. From the few short interviews I could find, he comes across as intelligent (as one would assume), but it’s hard to get much of an insight beyond that.

Jaideep Paul has been CFO since 2014. Before, he was the CFO of Airtel Nigeria, and he has 18 years of financial experience in the telecoms industry. On earnings calls, he comes across as very competent, with an intimate knowledge of Airtel’s numbers (including some of the more obscure ones).

Compensation is reasonable – for the CEO in FY23, minimum was $1.4m, target was $3.9m and actual was $2.4m; for the CFO $0.8m, $2.1m and $2.2m. Total comp is tied to a combination of revenue, EBITDA, OFCF, KPIs and stock return – fairly standard.

I look forward to reading Taldar’s first message to shareholders and seeing how he responds to questions on the next earnings call (assuming he’s on it), as this is usually the best way to gauge management quality.

Risks

Regardless of how many DCFs you run or how well you understand the financials, if you don’t understand the likelihood and severity of a business’s risks, you should not own their shares. It goes without saying that Africa is a high-risk area to invest. Political and economic instability abound, and fraud and corruption are rampant. Financial risk is elevated as lenders may be or become less willing to lend to African companies, and poorer-quality regulation introduces additional regulatory risk too.

Political and Economic Risk

Principal economic risks include exchange rate, inflation, and commodity price risk, all of which are closely linked. African countries are often overly dependent on a limited number of raw materials exports, especially oil, and we’ve already covered what can happen to exchange rates when the price of those exports falls. A weaker currency then induces inflation, as imports become more expensive. Arguably the biggest risk here is runaway inflation - there have been several examples of hyperinflation in sub-Saharan Africa in recent history, and several such countries, including Zimbabwe and Sudan, saw CPIs more than triple in 2023. Of AAF’s markets, the highest inflation rates in 2023 were seen in Nigeria (29%), Malawi (35%) and DRC (19%).

On the political side (excl. regulatory, which is covered later), my main concern is the possibility of government intervention/nationalisation/expropriation of assets. Unfortunately, this is one of those black swan-type risks which is incredibly hard to quantify. Sensible governments should realise that the increase in revenues from forcibly taking over a private enterprise is far outweighed by the loss of investor confidence such a move would cause, but relying on African governments to behave sensibly has not always yielded fantastic results historically.

However, Airtel Africa does have certain characteristics which reduce its political and economic risk, relative to other African companies. First and foremost is a diverse revenue base. The Naira situation exemplifies this - a telecom which operates only in Nigeria would be in a very rough spot at the moment, especially if it had significant non-Naira debt, but AAF’s net debt to EBITDA has barely budged. It also significantly lessens my concern about that black swan takeover risk, as the loss of any single market (with the possible exception of Nigeria) would not be impactful enough to change my thesis on AAF. Of course, the 14 markets in which AAF operates are not uncorrelated, and economic problems in one country may spread to others; but I feel much more comfortable than I would if I owned a business with all its operations in one African country.

Fraud Risk

The big question here is, how likely is it that Airtel Africa is materially misstating its financials?

Sub-Saharan Africa is certainly perceived as a higher-risk area in terms of corporate fraud. A notable example is Steinhoff, a South Africa-based company which used a complex system of loans between various subsidiaries to inflate profits by a rather impressive total of $7.4b between 2009-2017.

Honestly though, I think the fear is overblown. Many similar fraud cases have happened in the US, EU, China and just about everywhere else an investor may care to look, and I’ve struggled to find evidence to suggest large-scale corporate fraud is significantly concentrated in Africa (that’s not to say it definitely isn’t - if anyone has evidence to the contrary, or just disagrees, please do leave a comment).

Airtel Africa’s auditor is Deloitte, which does lend an additional modicum of credibility. Also, it’s important to remember that Airtel Africa is just a subsidiary of the much larger Bharti Airtel, the 8th largest company in India by market cap. Any major fraud would almost certainly require the involvement of high-level Bharti execs as well, which just seems unlikely to me.

Financial Risk

I’ve not talked much about their balance sheet so far, so I’ll give a rundown of the key points here (as of Dec 31, 2023):

Total borrowings - $2.33b. Breakdown is only reported annually, so as of March 31, this consisted of:

$550m of 5.35% senior notes due May 2024 (USD denominated)

$1262m of term loans ($722m within 1yr, $340m 1-2yrs, $534m >2yrs on undiscounted basis)

$361m of overdrafts, callable on demand

Lease liabilities (both operating and finance) - $1.77b. Maturity profile:

0-1yr: $572m, 1-2yrs: $545m, 2-5yrs: $912m, 5-9yrs: $468m, 9yrs+: $38m on undiscounted basis.Total cash & equivalents + other bank balances - $864m (note this does not include restricted cash of $735m pertaining to mobile money wallet balances)

The company expects to repay the $550m of notes that are coming due in May with cash on hand. Aside from these notes, their debt is 79% local currency, which reduces risk, as their revenues should move mostly in-line with their debt. They do pay a higher interest rate because of this - the average rate on the term loans and overdraft was 10.5% MRQ; but this is largely offset by expected currency depreciation.

As touched on earlier, Airtel Africa’s “leverage” (net debt to adjusted EBITDA) remained at 1.3x in MRQ despite the drop in Nigeria revenue, which is quite impressive - this may increase slightly over the first two quarters of calendar 2024 due to the further devaluation in February. However, it will remain well below the level of any debt covenants.

So all in all I think their financial risk to be fairly minimal.

Regulatory Risk

One of the key assumptions that my thesis for Airtel Africa depends on is that, broadly, currency depreciation will be balanced out by subsequent pricing increases by every operator, so the revenues are mostly agnostic of the exchange rate in the long run. This has generally been true so far - despite the large currency depreciations sub-Saharan Africa has seen over the past couple decades, MNO EBITDA margins remain well above the global average (40-50% vs 30-40% globally). However, in most of their markets, permission from regulators is required on any pricing changes or new plans, which introduces the risk of the government/regulator deciding to lower prices (or keep them flat during inflation) to gain popularity with their population.

This is currently most relevant in Nigeria. While the devaluation has not had an immediate impact on AAF’s margins (because their costs are mostly Naira), inflation is now bound to skyrocket, which will certainly pressure margins if the Nigerian Communications Commission refuses to allow price increases. The current CEO had this to say on the earnings call on Feb 1st:

“Our model is quite different, we don't use price to drive revenue accretion. We use two things, customer addition and usage growth. All of our activities are geared towards onboarding more and more customers, given the very low level of SIM penetration in our countries […] Of course if pricing comes, it's a sweetener, but we continue to engage the regulator on appropriate pricing, given the level of vision in Nigeria. Is it must-have? No. Is it a nice-to-have? Yes, and we’re going to continue to work with the regulator to make sure this happens.”

The NCC hired KPMG to conduct a cost-based study into mobile service pricing and recommend the best course of action - this is expected to conclude “imminently”, with KPMG recommending a tariff increase.5 Importantly, while a lack of price hikes would be a moderate hindrance to AAF’s margins, it would represent a potentially existential threat to competitors who haven’t shifted their costs to be Naira based (as mentioned earlier) so I think it’s unlikely that the regulator doesn’t raise tariff caps; and even if they remain at a low level for a few years, this may even benefit AAF in the long term as other operators would struggle to make the required 4G/5G investments.

In a similar vein to my argument regarding the risk of a government takeover, I’d suggest most African governments understand that the political benefit of the decrease in consumer expenses resulting from unreasonably low tariff limits is far outweighed by the decrease in investment that this incentivises, especially when they want to encourage more 5G investment; and pricing history supports this. But again, I’ll add the caveat that relying on African governments to make the sensible long-term decision (especially if there’s an election soon) may not always be a safe bet.

However, Airtel’s revenues are spread across enough countries that I’m quite comfortable with this risk.

Valuation

While I understand the value of a business to be the present value of all future cash flows, I don’t think an actual DCF adds any value in all but the most predictable of businesses (infrastructure, utility). I prefer to estimate a normalised earnings power, and only buy when the growth prospects, business quality and risk profile make it obvious that the business is undervalued, no excel required. There are just a few estimates we have to make before coming to a number:

Nigeria Projections

In FY23 (ended March ‘23), the Nigeria business did $2.13b in revenue. The constant currency growth rate is running at ~25%, and the currency has fallen ~70%. If the NCC raises the tariff cap 25%, that implies a current $1b revenue run-rate. While Naira appreciation seems more likely to me now than further depreciation, I’ll assume the rate remains flat for the sake of conservatism. I’ll also take the EBITDA margin to be 50%, lower than the MRQ 55%, to account for cost inflation in the next year.

Long-term Currency Depreciation

Currency depreciation rates affect the USD growth rate, but also change the value of locally denominated assets and liabilities, with depreciation actually being a positive in the latter case. This means for this earnings power estimation we actually get a bigger number out if we input higher depreciation. AAF estimate the “weighted average yearly potential devaluation” that they’re exposed to (calculated by taking the higher of 3 and 5 year historical devaluations) to be 7-8% per annum - we’ll use a more conservative 4%.

They have $1.42b in local currency debt, and about $920m in local currency leases not pegged to the dollar, according to the IR department. This implies an annual gain of $94m.

(Any losses on locally denominated cash & receivables are likely more than offset by local currency payables, since they typically have payables of ~$400m versus receivables of ~$150m.)

Interest Expense

In the most recent quarterly report, they reported their weighted average interest rate as 9.3%, which would imply $380m in interest per year. However, including finance charges they paid $127m in the quarter, which annualises to $508m.

I’m waiting to hear back from the IR team about this, and will update this post when I do. For the time being, I’ve taken it as $400m

Capital Expenditures

Airtel Africa is a capital intensive business. 5-year average capital expenditures (I’m using purchase of PPE + capital WIP + intangibles (spectrum) here, not capex as AAF defines it) of $950m significantly exceeds average D&A of $735m, owing to a heightened level of expenditure, especially in FY23, on 5G spectrum and data capacity (which doubled from FY21-FY23).

Buffett calculates owner earnings using maintenance capex, which he defines as the level of capex needed for a company to maintain its competitive position. Clearly, not all of that $950m was maintenance capex - they’ve been expanding their market share and are set to become the clear data leader with their 5G investments. However, maintenance capex still exceeds D&A. Currently, D&A is running at $800m; I think a fair conservative estimate for maintenance capex is $950m.

Estimating Earning Power

The only variables I haven’t covered are tax rate and non-controlling interests.

Their weighted-average national tax rate is 32.3%; tax on dividends from subsidiaries tends to contribute another 5%; and unreclaimable losses another 2.3%, for a reported effective tax rate of about 40%. While taxable income doesn’t include that $94m liability depreciation, this benefit is approximately offset by the difference between maintenance capex and accelerated depreciation, so 40% is used here.

Income attributable to non-controlling interests in Malawi, Rwanda and mobile money is at a run rate of $84m, flat YOY.

Therefore, the final headline figure for owner earnings attributable to shareholders is $518m. At the current share price of 94.4 GBp, this represents a multiple of 8.8.

Conclusion

Using a series of conservative estimates, we’ve arrived at a price to owner earnings of 8.8. This is for a business protected by strong barriers to entry, with immense long-term growth prospects, strong returns on capital, strong cash flow generation and the ability to reinvest large amounts of that cash flow at high rates of return. We’ll also likely see a shorter-term improvement in owner earnings as the Nigerian subsidiary recovers.

Their mobile money business alone - which is generating run-rate $440m annual EBIT, growing like nobody’s business, and requires virtually no capital to run - could conceivably be valued debt-free at several times Airtel Africa’s $4.55b market cap if only it were situated anywhere else.

So then what does the market see? Well, I’d be a fool to try and explain Mr Market’s manic-depressive reasoning, but in my view nowadays the market tends to price things based on segment, rather than a level-headed analysis of business prospects and risks. If we consider the segments that AAF sits within - telecom (capital intensive), Africa (scary!), high debt-to-equity (risky!) - it’s quite clear this is not a combination that would call for a high multiple. But is this business really so risky? They’ve just been through nearly a worst-case scenario, with the value of their biggest market’s currency dropping by more than 2/3rds, and their net-debt to EBITDA didn’t even increase. Compared to software/AI companies, many of which could have their lunch eaten by a competitor within a couple years with very little warning (I mean Jesus, look at SoundHound AI) yet still trade at sky-high multiples, I’m inclined to think not.

It may be months or it may be years before the market recognises the value here. I do not care. The longer the shares stay depressed, while the business continues growing (and paying a 4.6% dividend), the better the eventual return will be.

Aaaand with all that being said, I will still add this disclaimer - it’s Africa. Several of their key markets remain on the brink of default. The numbers could be fraudulent (“massaged”), or much of sub-Saharan Africa could have an economic meltdown, or a number of wars could erupt. It’s far from a safe bet, just one I think offers very asymmetrical risk/reward.

This write-up, and the research behind it, took many tens of hours over the course of a month and a half. If you enjoyed it, please do like the post and share with anyone you think may find it interesting; and drop any questions you may have in the comments below.

Also, if you haven’t already, you can subscribe to get roughly monthly posts like this emailed straight to you.

https://businessday.ng/analysis/article/explainer-what-is-nairas-fair-value/

https://businessday.ng/news/article/bank-of-america-says-naira-now-undervalued-after-float/

https://apnews.com/article/nigeria-oil-refinery-dangote-lagos-5e465512e5ed569512ea3221d0df2c79

https://nairametrics.com/2024/02/21/inflation-telecom-tariff-hike-imminent-as-operators-await-nccs-clearance/

https://nationaleconomy.com/telecom-operators-in-nigeria-anticipate-tariff-hike-amid-economic-strain/